The potential for Japan’s Nikkei 225 index to surpass its 1989 high after such a lengthy period is indeed a significant milestone, reflecting a notable recovery in Japanese stock markets. This achievement may evoke a sense of celebration among investors, especially those who have endured the prolonged period of stagnation.

However, it’s crucial to view this milestone within a broader context. While reaching previous highs can be a positive indicator of market sentiment and economic recovery, it does not necessarily imply that all underlying issues or challenges have been resolved. Japan still faces structural challenges such as demographic aging, deflationary pressures, and economic reforms, which could impact the sustainability of the market’s upward trajectory.

Additionally, focusing solely on index performance may overlook the diversity of individual stocks and sectors within the market. While certain sectors, such as technology, may be driving market gains, others may be lagging behind or facing headwinds.

Therefore, while the potential milestone for the Nikkei 225 is noteworthy, investors should approach it with a balanced perspective, considering broader economic factors, market dynamics, and their own investment objectives when making decisions. Diversification and prudent risk management remain crucial principles for long-term investment success.

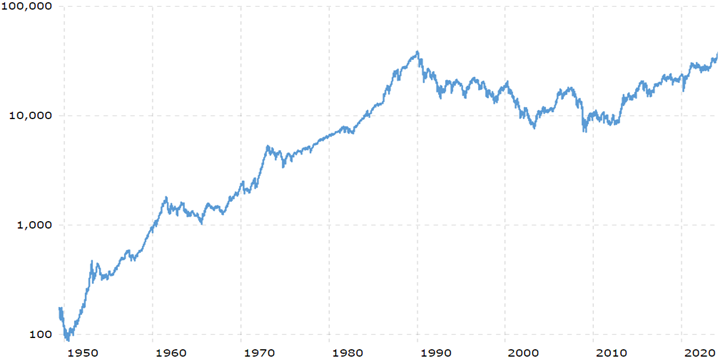

At the highest level, it is a sign of just how bad things have been, which isn’t something one usually celebrates. It’s more like a funeral than a birthday. Japanese stocks peaked on the last trading day of 1989, and the Nikkei went on to fall more than 80%.

Investors were crushed, with the Nikkei losing about as much—albeit over a longer period—as the precursor to the S&P 500 did from 1929 to 1933, during the Great Depression. It took the U.S. market a quarter of a century to make a new high.

| Year | Average | Year Open | Year High | Year Low | Year Close | Annual |

| Closing Price | % Change | |||||

| 1933 | 9.04 | 6.83 | 12.2 | 5.53 | 10.1 | 46.59% |

| 1932 | 6.92 | 7.82 | 9.31 | 4.4 | 6.89 | -15.15% |

| 1931 | 13.66 | 15.85 | 18.17 | 7.72 | 8.12 | -47.07% |

| 1930 | 21 | 21.18 | 25.92 | 14.44 | 15.34 | -28.48% |

| 1929 | 26.19 | 24.81 | 31.86 | 17.66 | 21.45 | -11.91% |

Less obvious but more important is that headline index numbers really don’t matter very much over long periods. The Nikkei, like the Dow Jones Industrial Average, is an atrocious way to gauge the market. Index numbers don’t include the dividends investors receive. They don’t count the pernicious impact of inflation. And measuring returns from the peak of one of the biggest bubbles in history tells us little about the future.

The Nikkei is a flawed measure. First created in 1950 by the eponymous newspaper, the Nikkei averages stock prices, so higher-price stocks have more impact than low-price ones. This is silly, since the price of a stock is an arbitrary result of how many shares the company chooses to issue—and just as with the Dow, it leads to some bizarre results.

Nikkei 225 Index

The largest constituent of the Nikkei is Fast Retailing, owner of the fashion chain Uniqlo, making up almost 11%. Toyota Motor, the country’s most-valuable company, makes up 1.4%. Rank stocks by their market value as other important indexes do, and Fast Retailing would be under 2% of the gauge and the seventh-largest component.

This could be laughed off, except for the fact that, unlike the Dow, the Nikkei really matters. Futures contracts based on it are far more widely traded than those based on the Topix, the better measure produced by the stock exchange. As a result, huge amounts of money move based on something not up to the job of helping decide how capital should be allocated among companies.

Use the Topix instead of the Nikkei, and stocks are still more than 8% below their December 1989 peak. So celebrations about a new price high are anyway premature.

Dividends are vital. Over the long run, the compounding effect of reinvesting dividends makes a huge difference to returns.

In the past half-century, U.S. stocks turned $100 into $6,200 without dividends (ignoring costs and taxes) while with dividends they would be worth $25,000. The same is true in Japan, where the 2% yield from dividends is now much higher than in the U.S.

An investor who made the dire decision to buy at the top of the bubble and reinvest dividends made back all losses by March 2021. Somehow we forgot to hold a party.

Inflation matters, too. The good news for asset owners in Japan is that a decade and a half of deflation meant stuff got cheaper, so during that supposed “lost decade” the value of their assets wasn’t eroded by inflation, as it was elsewhere.

The bad news is that returns were way higher everywhere else even after inflation. Worse, inflation before and after the lost decade has left the after-inflation value, excluding dividends, of the Nikkei (and Topix) still substantially below the 1989 peak.

Japanese investors didn’t even get a stronger currency—which usually comes with deflation—as compensation: The last decade of stimulus in the country weakened the yen back to roughly where it was at the peak of the 1989 bubble.

Read Original Article At The WallStreet Journal